The Liability Dilemma Before the Commercialization of Autonomous Driving

Introduction

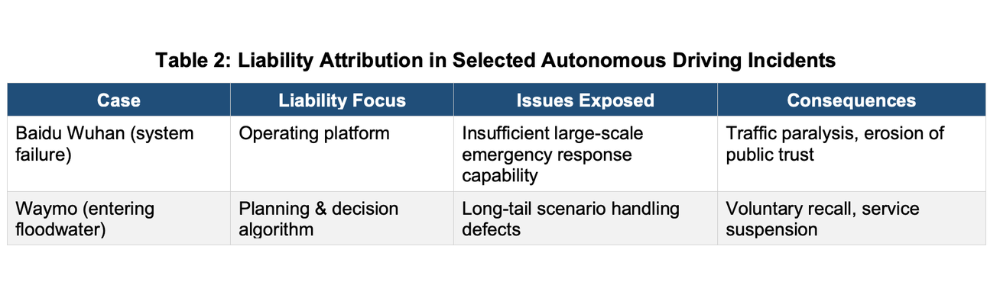

This year, the robotaxi industry has witnessed two incidents that have attracted considerable attention. On March 31, Baidu’s Apollo Go experienced a large-scale system failure in Wuhan, with more than 100 vehicles simultaneously coming to a halt in the middle of major thoroughfares, severely disrupting traffic order. Just one month later, Waymo’s autonomous vehicles in San Antonio and Atlanta drove into severely flooded roadways, causing the vehicles to become stranded and ultimately triggering a voluntary recall of nearly 3,800 vehicles along with the temporary suspension of services in parts of certain cities.

Meanwhile, 2026 has been dubbed the inaugural year of autonomous driving commercialization. Taking China’s Pony.ai as an example, its Robotaxi business revenue in the first quarter grew 395.4% year-over-year, while passenger fare revenue surged 456.5%.

As the commercialization of autonomous driving accelerates toward scaled operations, clearly delineating the responsibilities of all stakeholders has become an unavoidable core issue for the industry. Without clearly defined liability rules, insurers risk protracted disputes when handling claims, while banks face heightened uncertainty in valuing autonomous driving assets and assessing credit risk. Drawing on publicly available cases, this article examines the regulatory environments and liability attribution practices for autonomous driving across different jurisdictions and explores the implications of these experiences for Hong Kong’s financial technology and regulatory landscape.

This article argues that clear liability frameworks are essential for the scaled commercialization of autonomous driving. When responsibility cannot be effectively allocated among manufacturers, algorithm providers, and operating platforms, the financial system struggles to provide deterministic risk protection. Hong Kong, as an international financial center, is well positioned to serve as a regional hub for autonomous driving risk management and insurance innovation, even if it does not lead in the underlying vehicle technology itself.

Part I: Observations on Divergent Regulatory Pathways for Autonomous Driving

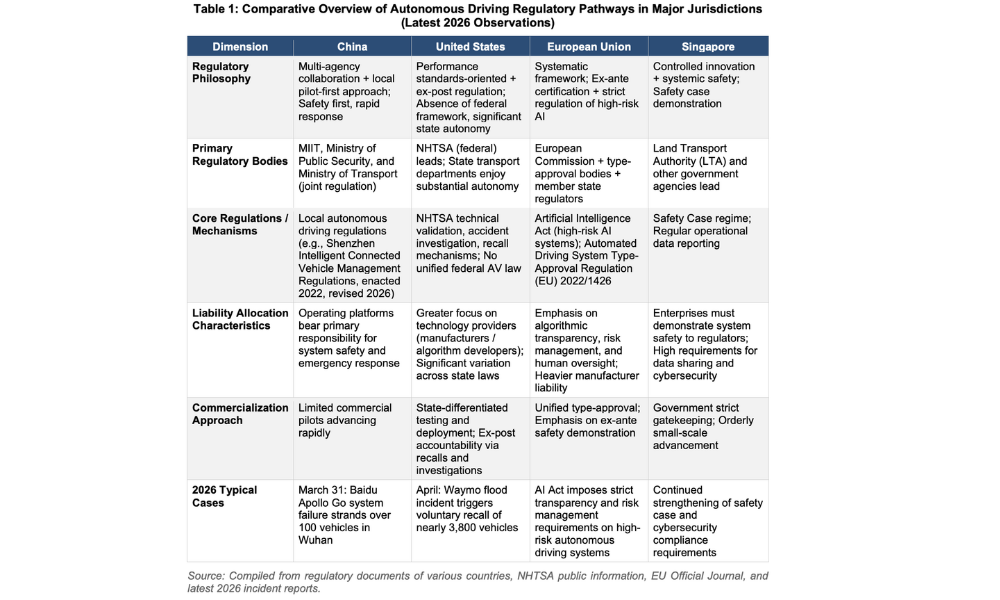

Global regulatory pathways for autonomous driving currently vary significantly across jurisdictions. This article takes China, the United States, the European Union, and Singapore as illustrative examples:

China adopts a multi-agency collaborative model with local pilots taking the lead. Oversight is primarily exercised jointly by the Ministry of Industry and Information Technology (MIIT), the Ministry of Public Security, and the Ministry of Transport. The approach emphasizes safety-first principles and rapid response mechanisms and currently relies mainly on local regulations. In practice, operating platforms typically bear the primary responsibility for system safety and emergency response, while some cities have begun exploring limited commercial operation pilots.

The United States favors a performance standards-oriented, ex-post regulatory approach. At the federal level, a unified regulatory framework is still absent. The National Highway Traffic Safety Administration (NHTSA) primarily regulates through technical validation, accident investigation, and recall mechanisms, with liability attribution more heavily focused on technology providers. Individual states enjoy substantial autonomy, resulting in marked variations in regulatory rules.

The European Union has developed a relatively systematic regulatory framework, anchored by two core pieces of legislation: the Artificial Intelligence Act, which classifies autonomous driving systems as high-risk AI systems and imposes requirements for algorithmic transparency, risk management, and human oversight; and the Automated Driving Systems Type-Approval Regulation (Regulation (EU) 2022/1426), which establishes unified type-approval procedures and technical requirements while emphasizing ex-ante safety demonstration.

Singapore’s regulatory style prioritizes controlled innovation and systemic safety. Enterprises must demonstrate system safety to regulators via safety cases and submit regular operational data reports, while facing stringent requirements regarding data sharing and cybersecurity.

To present the differences in regulatory pathways among the four jurisdictions more clearly, the following comparison examines regulatory philosophy, core mechanisms, liability allocation characteristics, and 2026 latest practices (see Table 1). These divergent approaches set the stage for the liability challenges discussed in subsequent sections.

Part II: The Core Challenges of Moral Dilemmas and Liability Attribution

Autonomous driving transfers the moral decision-making previously borne by human drivers to algorithmic systems, thereby giving rise to profound moral dilemmas. The most representative example is the classic “trolley problem” transposed into the autonomous driving era: when a system faces an unavoidable accident, how should the algorithm weigh the relative value of different lives or interests?

The Algorithmic Trolley Problem: Moral Preferences and Public Trust

The MIT Media Lab’s 2018 “Moral Machine” study, drawing on more than 40 million decision datapoints from 233 countries and regions, provided the first large-scale empirical response to this question. The study identified three strong common global preferences: prioritizing the protection of humans over animals, saving more lives rather than fewer, and saving younger people rather than older people. However, cultural differences proved even more striking.

The “Eastern cluster,” represented by China and Japan, exhibited a significantly weaker preference for prioritizing the protection of younger people compared with Western countries — a pattern potentially linked to the Confucian cultural tradition of “respecting the elderly.” In contrast, the “Southern cluster,” represented by France and Latin American countries, showed the weakest preference for protecting humans relative to pets.

These differences imply that no single autonomous driving moral algorithm can be universally applicable across global markets. Should an algorithm design in a given region fail to reflect the specific moral preferences of the local public, any accident could trigger a collapse in public trust in the technology and legal recourse pressures far exceeding what technical explanations alone can address.

This further complicates liability attribution: when an algorithm makes a decision based on a particular moral preference (for example, sacrificing older individuals to protect a greater number of people), does responsibility rest with the designer who followed majority intuition, or with the operator who failed to anticipate that such a decision would provoke controversy? The “black box” character of algorithmic decision-making renders its logic difficult for outsiders to comprehend and simultaneously erodes public trust in the system.

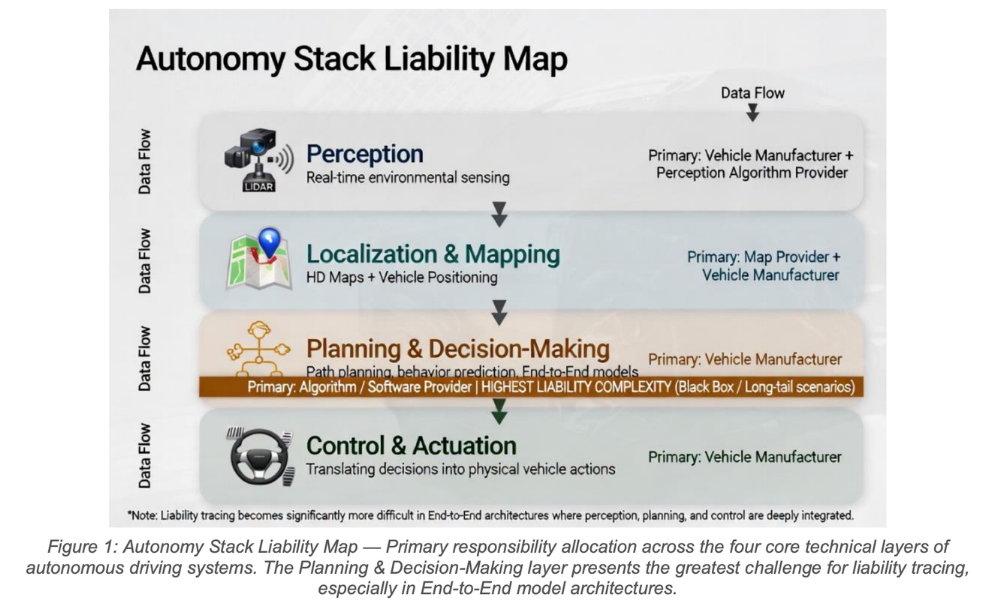

Decomposing Liability Across the Autonomy Stack

This article decomposes autonomous driving, according to first principles, into four core technical components and examines the attribution of responsibility for each:

1. Perception

Responsible for the real-time, accurate acquisition of surrounding environmental information. If sensors fail or recognition errors occur in complex environments, primary responsibility typically lies with the vehicle manufacturer or the perception algorithm provider. Operating platforms bear responsibility for the routine maintenance and calibration of sensors; however, when perception errors lead to accidents, liability must often be apportioned between the technology provider and the operator.

2. Localization and Mapping

Responsible for determining the vehicle’s own position. If high-definition (HD) map data contains errors or the positioning system fails, responsibility usually involves both the map provider and the vehicle manufacturer. Operating platforms, meanwhile, must bear responsibility for map updates and maintenance as well as the day-to-day management of the positioning system. Mainstream L4 systems still widely rely on HD maps, yet some autonomous driving developers are exploring technical routes that reduce map dependency, rendering the delineation of map-related liability increasingly complex.

3. Planning and Decision-Making

Responsible for generating driving decisions on the basis of perception and localization information. This is the component in which liability tracing is most difficult. When defects appear in the algorithm’s decision logic within long-tail scenarios, core responsibility falls upon the software and algorithm provider. In recent years, a growing number of companies have adopted End-to-End models that deeply integrate perception, planning, and decision-making, directly outputting control commands from sensor data. While such architectures may enhance overall performance, they also render the intermediate decision-making process highly opaque, further increasing the difficulty of liability tracing.

4. Control and Actuation

Responsible for translating decisions into the vehicle’s physical actions. If actuators malfunction, primary responsibility rests with the vehicle manufacturer. Operating platforms must ensure that vehicles remain in good working condition; however, when execution errors become intertwined with upstream perception or decision errors, liability apportionment becomes considerably more complex.

Actual cases illustrate these liability differences more clearly:

Different regulatory environments produce varying emphases in liability attribution, yet both confront the common challenges of the “technical black box” and “dispersed responsibility.” When liability can be perpetually shifted among manufacturers, software providers, and operating platforms, the financial system struggles to furnish any party with deterministic risk protection. Insurance pricing and risk assessment consequently face significant difficulties.

Part III: The Impact of Liability Attribution on Insurance and Finance

When liability attribution mechanisms remain imperfect, they exert material effects on both the insurance and financial systems. As autonomous driving enters scaled commercial operations, these effects are moving from theoretical discussion to practical operational reality.

In the insurance sector, traditional motor insurance has long centered its pricing logic on “human fault.” Yet when an accident may involve multiple stakeholders — vehicle manufacturers, software algorithm providers, operating platforms, and others — existing liability models struggle to define claims responsibility and apportionment with clarity. For instance, should a robotaxi collide during operation and injure passengers inside the vehicle, pedestrians outside, or occupants of other vehicles, current guidance is lacking on whether insurers should pay out first and subsequently pursue recourse, or simply decline the claim. This ambiguity directly impairs the effectiveness of traditional actuarial models built on historical data and human responsibility.

Insurers therefore face substantial uncertainty in evaluating their risk exposure, often resulting in conservative pricing or inadequate product availability. At the same time, demand is rising for new insurance products such as product liability, operator liability, and cybersecurity coverage; however, the absence of clear liability delineation standards continues to hinder the design and pricing of these products.

As autonomous driving technology advances, unclear liability attribution is likely to pose ongoing challenges for insurance pricing. Future efforts could explore differentiated pricing mechanisms that incorporate assessments of system transparency and verifiability. Referencing, for example, the EU Artificial Intelligence Act’s requirements for transparency in high-risk AI systems, it may become feasible to differentiate premium rates according to the degree of risk verifiability, thereby supplying insurers with a more scientifically grounded pricing reference.

For the banking sector, the difficulty of risk assessment and credit approval for autonomous driving-related assets has increased markedly. Novel asset classes — vehicle fleets, algorithmic software, and operational data — lack mature valuation and risk-pricing models, rendering traditional risk-assessment frameworks centered on tangible assets and stable cash flows difficult to apply directly. Because of significant uncertainty surrounding accident liability attribution, banks struggle to accurately gauge enterprises’ asset-recovery capacity in default scenarios. This lack of reliable inputs for loss-given-default estimation leads to more cautious credit decisions.

In the current environment, banks prefer to participate in related projects indirectly — through supply-chain financing, policy-based lending, or partnerships with vehicle manufacturers — rather than extending large-scale direct credit to purely technology-driven autonomous driving enterprises. Furthermore, the actual value of a remotely upgradable autonomous vehicle may change substantially following a single over-the-air (OTA) update, posing fresh challenges for banks’ collateral management and risk-mitigation practices.

At the same time, unclear liability attribution has created new development opportunities within the RegTech domain. Demand for technologies such as event data recording, algorithm auditing, and real-time risk monitoring is growing rapidly. Hong Kong possesses recognized strengths in FinTech and RegTech and is well positioned to contribute in this emerging arena. In particular, the development and deployment of standardized Event Data Recorders (EDR), algorithm black-box audit platforms, and real-time risk-scoring systems can help enterprises meet regulatory requirements more effectively while simultaneously furnishing insurers with more precise risk-assessment tools.

Overall, the lag in liability attribution mechanisms is becoming one of the principal constraints on the commercialization of autonomous driving. It not only elevates uncertainty in insurance pricing but also heightens risk-management challenges for financial institutions. Only by forging effective linkages between technological progress and clear liability attribution can the financial system provide stable support for this nascent industry.

Part IV: Implications for Hong Kong’s FinTech and Regulatory Landscape

As an international financial center, Hong Kong faces both challenges and opportunities in the domain of autonomous driving liability. Unclear liability attribution may increase risk-management difficulties for local insurers and banks; simultaneously, it opens space for Hong Kong to leverage its RegTech strengths and drive innovation in financial products.

The Insurance Authority (IA) can play an active role in this process. Hong Kong has not yet issued specific liability guidelines for autonomous driving. Whether a localized autonomous driving liability framework should be developed merits joint examination by regulators and industry participants. Such a framework would not only help clarify liability division within the local market but also furnish a clearer rule base for cross-border operations.

In drawing on international experience, Hong Kong can reference liability-allocation practices from different jurisdictions and explore a regulatory framework suited to local conditions. Singapore’s model — combining a safety-case regime with government-led risk control — has enabled the orderly advancement of autonomous driving while safeguarding safety; its experience is reflected not only in regulatory design but also in the strategic transformation from financial center to insurance center. The European Union’s emphasis on algorithmic transparency and ex-ante certification raises the bar for system verifiability. The United States’ performance-standards and ex-post regulatory model has accumulated substantial practical experience in liability tracing. Hong Kong can selectively incorporate the most appropriate elements of these approaches in line with its own positioning.

Singapore Case Study: From Financial Center to Autonomous Driving Insurance Hub

Singapore’s experience offers Hong Kong the most directly relevant reference. Since 2017, the Land Transport Authority (LTA) has operated a regulatory sandbox encompassing testing, deployment, and insurance. All autonomous vehicles are required to carry mandatory third-party liability insurance. In 2025, Allianz Insurance underwrote a customized policy for WeRide’s driverless shuttle service operating in Sentosa — the world’s first such operation without an on-board safety operator. The policy covers sensor damage and third-party liability and incorporates real-time risk monitoring based on driving data. By early 2026, the service had completed several thousand safe journeys.

The key lesson is that Singapore did not wait for full commercial maturity before acting. Regulatory authorities established safety-certification and insurance frameworks in advance, while insurers concurrently developed products tailored to different levels of automation. Hong Kong can use this approach, combining it with cross-border Greater Bay Area scenarios, to explore the possibility of becoming a regional hub for autonomous driving insurance.

Practical Priorities for Hong Kong

On the practical front, Hong Kong can concentrate on the following priorities:

- Insurance Product Innovation: Unclear liability attribution remains the principal obstacle to effective insurance pricing. Future work should explore differentiated pricing mechanisms that factor in assessments of system transparency and verifiability. Products covering sensor damage, algorithmic failure, and cyber incidents should be developed in close coordination with regulators.

- RegTech-Enabled Cross-Border Compliance: Building on its existing capabilities in FinTech and RegTech, Hong Kong can advance the research, development, and application of tools such as standardized Event Data Recorders (EDR), algorithm black-box audit platforms, and real-time risk-scoring systems, thereby helping enterprises navigate compliance obligations across multiple regulatory regimes (Mainland China, EU, US, and ASEAN).

- Positioning as a Regional Risk-Control Hub: Banks, insurers, and FinTech firms in Hong Kong should proactively develop capabilities in risk assessment and product innovation, strengthen communication and coordination with mainland Chinese and international regulators, and monitor collaborative opportunities arising from autonomous driving development in the Greater Bay Area. Shenzhen, Guangzhou, and other cities are already conducting autonomous driving tests. By capitalizing on its financial and insurance strengths, Hong Kong can explore becoming a regional “insurance and risk-control center,” supplying risk-management support for the broader development of autonomous driving across the Greater Bay Area.

Hong Kong need not become a technological pioneer in autonomous driving itself, yet it is fully capable of serving as a global hub for the risk management of this technology. Through institutional innovation and the application of technology, Hong Kong has the potential to play a distinctive role in this emerging field.

Conclusion

The contrasting experiences of Baidu and Waymo under different regulatory regimes demonstrate that unclear liability attribution has become a critical constraint on the commercialization of autonomous driving. When accident liability involves multiple stakeholders — manufacturers, software providers, and operating platforms — the traditional human-centered logic of liability allocation is no longer fit for purpose.

Ambiguous liability attribution affects not only technological deployment but also transmits directly into financial domains such as insurance pricing and risk management. Insurers struggle to assess risk exposure with precision, while banks lack reliable foundations for asset valuation and credit decisions, thereby limiting the financial system’s ability to support this emerging industry.

As an international financial center, Hong Kong — while not necessarily a technological frontrunner in autonomous driving — is well positioned to serve as a bridge and innovator in liability attribution, insurance innovation, and risk management. By drawing on the experiences of diverse jurisdictions, Hong Kong can develop a liability framework suited to its own context and harness its RegTech strengths to help enterprises navigate cross-border compliance challenges. Leveraging the advantages of autonomous driving testing in the Greater Bay Area, Hong Kong is poised to evolve gradually into a regional “insurance and risk-control center.”

Faced with a technological transformation that is reshaping both transportation and financial landscapes, relevant institutions should adopt a responsible, innovative, and pragmatic stance — proactively studying and addressing the risks and opportunities presented by this emerging domain. When the steering wheel no longer belongs to any individual, responsibility nevertheless endures. Whoever underwrites the risk ultimately commands the pricing power of future finance.

Data and Case Sources

U.S. National Highway Traffic Safety Administration (NHTSA) public accident and recall archives; EU Official Journal (Artificial Intelligence Act and Regulation (EU) 2022/1426); Singapore Land Transport Authority (LTA) regulatory documents; Baidu and Waymo official announcements; Pony.ai Q1 2026 earnings report; Allianz Insurance Singapore branch press releases; MIT Nature paper (Awad et al., 2018); and media reports from Reuters, The Straits Times, China News Service, and others covering 2025–2026.